When prices rise and markets shift, even small financial decisions start to feel risky. People want to protect what they’ve earned, but not every option feels safe or clear. Knowing where to keep your money can make a big difference in how secure you feel day to day. Explore 10 smart ways to hold your money with confidence and stay steady when the economy feels shaky.

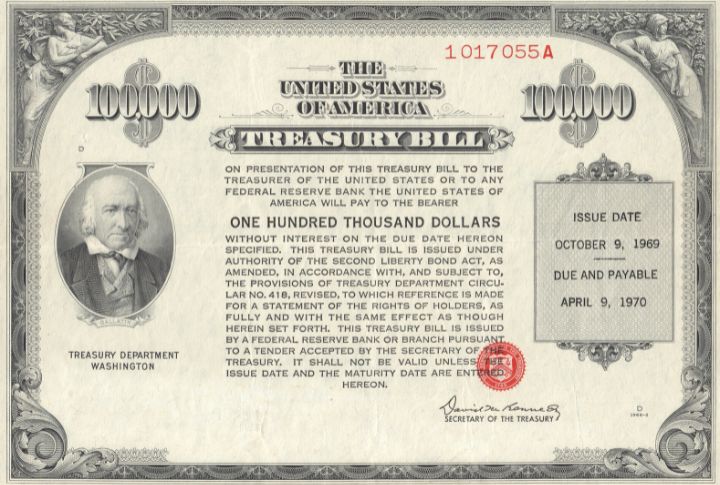

U.S. Treasury Securities: The Ultimate Safe Haven

When the economy feels uncertain, people often look to U.S. Treasury bonds. These securities are backed by the full faith of the United States, making them among the most reliable options available. Such assets are also quite simple to sell if a person ever needs to. The nation has never failed to pay on time.

Treasury Inflation-Protected Securities (TIPS): Safety With Inflation Hedge

To guard your savings against rising prices, you can use TIPS. Backed by the government, they carry a very low chance of losing value. Their principal adjusts as prices go up, and keeps your purchasing power protected. Just know they don’t perform well during low-inflation periods.

High-Yield Savings Accounts: Safe Liquidity With Competitive Returns

Putting money into a high-yield savings account gives you instant access to your funds without any penalties. This capital is protected by federal insurance up to $250,000, so it remains shielded from bank failure. Current interest rates are often much better than traditional accounts, which helps your resources grow steadily and securely.

Certificates Of Deposit (CDs): Fixed Returns With Guaranteed Safety

Certificates of Deposit, or CDs, provide a safe way to earn a fixed return over a set period. An account is federally insured with a limit of $250,000, and that protection reduces the chance of losing the main investment. Although penalties for early withdrawal exist, they also motivate you to hold onto these savings for the full term.

Money Market Funds: Stability Plus Liquidity

You can invest in these funds to own a piece of many short-term government assets and other high-quality business debt. They generally have very low risk compared to stocks or long-term bonds. A major advantage is the easy access to the funds, frequently without a penalty. A basic checking account usually delivers lower returns compared to funds of this type.

Precious Metals: Tangible Store Of Value In Economic Downturns

Putting money into real assets like gold and silver can be a safe strategy during currency fluctuations. Metals like silver and gold have intrinsic value and work as protection against inflation and weakening currency. Their prices don’t usually move with stocks, which can make a person’s overall portfolio more diverse.

Stable Value Funds: Capital Protection In Retirement Accounts

In retirement plans like a 401(k), you can find funds created for capital protection. They invest in quality bonds and insurance contracts, promising to guard your main investment while providing a consistent return. These are a less volatile alternative for your retirement savings, particularly if you are approaching retirement.

Inflation-Protected Annuities: Guaranteed Income That Keeps Pace

If you’re worried about your retirement income keeping up with inflation, such annuities can provide a solution. These annuities provide a stream of income that increases alongside rising prices. With insurance companies as backing, they provide a stable and predictable source of funds to enhance retirement income.

Short-Term Municipal Bonds: Tax-Advantaged Safety

These bonds are issued by local governments and often have high credit quality. They provide interest income that is usually free from federal taxes, and at times, state taxes as well. The short maturity of certain bonds means less risk from shifting interest rates and provides a stable, tax-efficient way to earn.

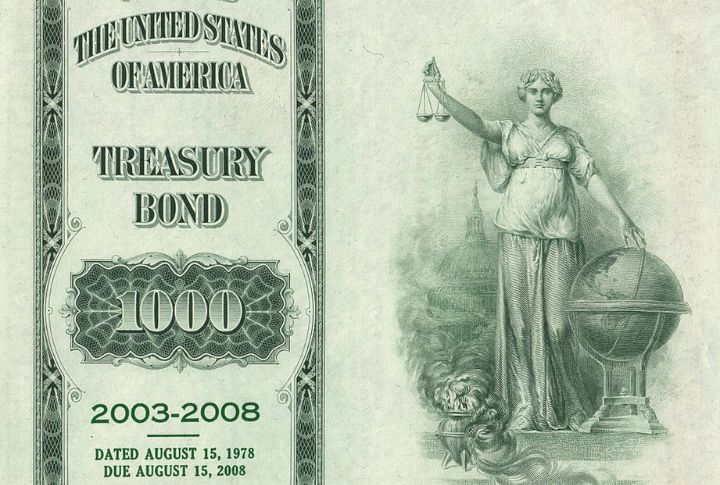

Diversified Treasury Bond Funds: Broad U.S. Government Exposure

Rather than buying individual bonds, you can invest in a fund that holds a variety of U.S. Treasury bonds. This approach offers a consistent income backed by the U.S. government while also spreading your risk across different maturities. It is also a much more accessible way to own government debt.