Credit cards can feel easy until interest stacks up like laundry you meant to fold some days ago. The fix isn’t cutting them out, but knowing how to handle them the smart way. These 10 ways break down how to avoid debt and build strong credit without stress. Keep scrolling and take control of your spending with confidence and clarity.

Always Pay More Than The Minimum Due

Only paying the minimum each month traps you in long-term debt, especially with APRs hovering around 20%. Many banks highlight the minimum to subtly encourage low payments. Paying more each cycle reduces long-term interest and substantially shortens the time it takes to pay off.

Set Up Automatic Payments

Late fees and credit score drops hit hardest after missed payments. Autopay handles bills reliably and reduces stress. You can set it to cover the full statement balance, helping prevent compounding interest. Smart automation means fewer errors and steadier financial control.

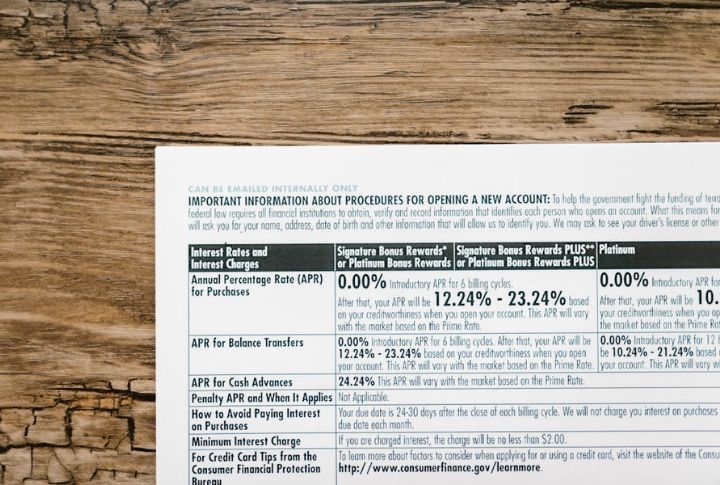

Know Your Interest Rate (APR)

Understanding the APR is essential. Cards typically carry variable APRs, with many hovering near 25%. Missing one payment can cause rates to rise even higher. Comparing options and tracking terms helps avoid hundreds of extra costs annually. Awareness here prevents financial traps.

Avoid Cash Advances

Interest begins the moment you take a cash advance. With fees up to 5% and APRs exceeding 29%, it’s one of the most expensive credit moves. ATMs make it tempting, but the price is steep. Use alternatives like savings or debit instead.

Keep Your Credit Utilization Under 30%

Using less than 30% of your available credit demonstrates to lenders that you manage debt wisely. High utilization can hurt your score and trigger financial scrutiny. Many top scorers stay under 10%. Another smart move is to request a credit limit increase to instantly reduce your ratio.

Don’t Co-Sign Cards For Others

It is risky to take responsibility for someone else’s spending. Co-signed cards affect both parties’ credit history and open the door to default damages. Even if you’re not using the card, it will still appear on both your reports. Removal is rare, and regrets are common.

Never Ignore Your Billing Cycle

Your billing cycle directly affects payment timing and reported balances. When you plan purchases after the cycle closes, it can offer nearly two months of float. Paying early improves reported utilization, and knowing this rhythm helps you dodge fees and maximize grace periods.

Watch Out For Introductory Offers

Credit card teaser rates usually last between 6 and 21 months—after that, the APR often jumps significantly. If you miss a payment, you may lose the promotional rate immediately. Also note that balance transfers come with upfront fees. While these offers can save you money, they only do so if you stay updated.

Check Your Statement For Errors

Checking your credit card statement regularly helps you catch fraud and fix mistakes before they grow. Federal law gives you just 60 days to report errors, so timing matters. Even small duplicates can add up quickly, but routine reviews help protect your credit and maintain a clean credit history.

Avoid Store Credit Cards

The biggest drawback of retail credit cards is that they may only be used at the designated retailer, and they frequently have interest rates higher than 29%. Add to that hidden fees that leave many customers with regrets. While the upfront discount may seem appealing, it rarely offsets the long-term drawbacks.