Earning a modest income raises practical questions about the future. And Social Security sits at the center of those concerns because it acts as the safety net most people rely on later in life. The amount you earn directly shapes what eventually comes back. For someone bringing in $25,000 a year, the outcome is fairly predictable. Let’s unpack how those earnings translate into benefits and what that means for your financial stability.

Average Indexed Monthly Earnings (AIME)

Your Social Security story begins with Average Indexed Monthly Earnings, or AIME. It’s calculated by looking at the 35 highest-earning years, adjusting them for inflation, and then dividing by 12. If you worked fewer than 35 years, those missing years count as zeros.

Working Fewer Than 35 Years

Adding to that, to avoid pulling the average down, working even part-time or lower-paying jobs can help replace those zeros with positive amounts. Reviewing your earnings through a My Social Security account ensures better planning and stronger benefits.

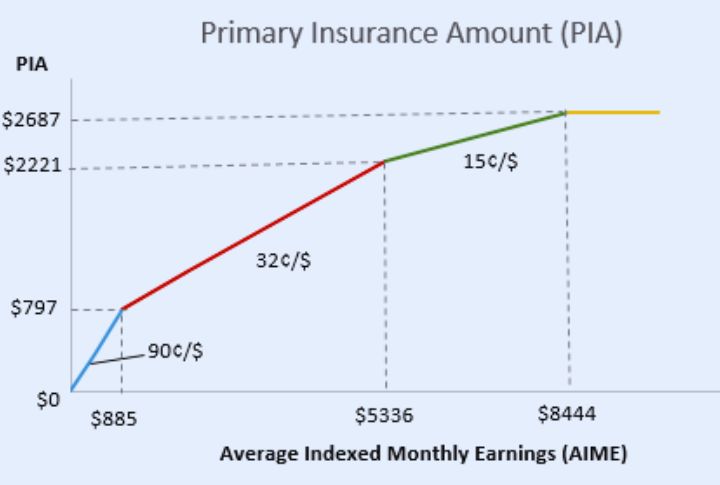

Primary Insurance Amount (PIA)

Monthly benefits at full retirement age come from the Primary Insurance Amount, or PIA. This figure is built using AIME and a tiered formula. Portions of your earnings are multiplied by 90%, 32%, and 15%, producing the base benefit that shapes your Social Security check.

Bend Point Formula

Benefit amounts depend on bend points, which create the stepping stones in Social Security’s formula. As of 2025, the levels are $1,226 and $7,391. Earnings up to either of these thresholds are multiplied by 90% and 32%, while anything beyond the upper mark receives only 15%.

Full Retirement Age (FRA)

Full Retirement Age is the milestone when you receive the entire Primary Insurance Amount without reductions. Depending on your birth year, it ranges between 66 and 67. Identifying this age matters, since it signals when Social Security begins paying the full monthly benefit.

Early Claiming At Age 62

You may choose to start collecting Social Security at 62, the earliest option available. But doing so reduces your monthly benefit permanently, often by more than 25% compared with waiting until full retirement age. Even with the reduction, many retirees still choose to begin benefits early.

Delaying Benefits Past FRA

Monthly benefits can reach as high as $5,108 in 2025 for those with the highest earnings. Waiting beyond Full Retirement Age adds predetermined increases to that amount each year. By delaying until 70, retirees maximize their payout through Social Security’s growth mechanism.

Maximum Monthly Benefit

So, for workers earning $25,000 annually, smart benefit timing becomes important since reaching Social Security’s maximum payout of $5,108 monthly isn’t possible without 35 years of peak earnings. Yet these earners can wait until 70 to capture a valuable 76% boost in monthly benefits.

Cost-Of-Living Adjustment (COLA)

Fixed incomes face a constant threat from inflation’s erosive effects, but Social Security has built-in protection through its cost-of-living adjustment (COLA). This systematic safeguard recalibrates benefit amounts each January based on inflation levels announced the previous fall. It helps maintain recipients’ purchasing power even as prices climb over time.

Increasing Earnings Later In Career

Here’s a little-known perk of Social Security: benefits are automatically recalculated when higher-income years appear in the record. Crossing the $25,000 mark later in your career can replace weaker periods within the 35-year average. This means that even a single stronger year has the potential to increase future payments.