The Great Depression shattered illusions of American prosperity, and the middle class, once confident in its financial security, was hit hardest. Unlike the poor, who were accustomed to instability, or the rich, who had buffers, the middle class had no safety nets in place. These 10 critical missteps reveal why so many were caught off guard.

They Lacked An Emergency Fund

Many households had no reserves set aside when wages disappeared. When they were suddenly unable to pay rent or afford food, they turned to credit for temporary relief. However, debts accumulated quickly, and without public safety nets to rely on, the lack of savings soon led to lasting financial hardship.

They Underestimated The Length Of The Crisis

Some believed the downturn would resolve within months and resisted long-term adjustments. They clung to old spending patterns or paused job searches, assuming things would rebound quickly. That optimism faded slowly, replaced by desperation. As the years wore on, early inaction left them with fewer tools to manage adversity.

They Failed To Diversify Investments

Stock investments became the main strategy for building wealth. When the market crashed, so did personal savings. Those without other assets had no fallback. Entire fortunes vanished in hours, and with no portfolio diversity to soften the blow, recovery was nearly impossible once the financial system began to fail.

They Ignored Government Assistance Programs

Reluctance to seek help kept families in preventable hardship. Relief was often viewed with suspicion or resisted out of pride, even as programs like the New Deal became available. That hesitation led to uneven uptake, and by the time many acted, the window for avoiding deeper, longer-lasting suffering had passed.

They Did Not Adjust Spending Habits Quickly

In the early months, some families continued to spend as if nothing had changed. However, as conditions worsened, budgets collapsed. Because reductions came too late, savings were already depleted. This delayed adjustment left families with fewer resources precisely when careful spending became a financial necessity.

They Failed To Seek Alternative Income Sources

Many expected lost roles to return, so they delayed making changes. As the economy shifted, this delay became costly. Freelance opportunities were missed, and reskilling felt out of reach. Those who adapted sooner stayed afloat, while those who waited faced longer periods of uncertainty.

They Had Overcommitted To Mortgages

Confident in rising earnings, buyers took on larger mortgages than they could sustain. They expected steady incomes to cover the cost. But when layoffs and wage cuts followed, those expectations fell apart. Foreclosures surged, stripping families of both homes and security. What once signaled success became a source of lasting strain.

Neglecting Self-Sufficiency

Unlike rural households, most middle-class city dwellers lacked basic survival skills. With food prices rising and cash scarce, their total reliance on purchased goods became a major weakness. This group rarely grew vegetables or preserved food, and few knew how to manage without constant access to stores.

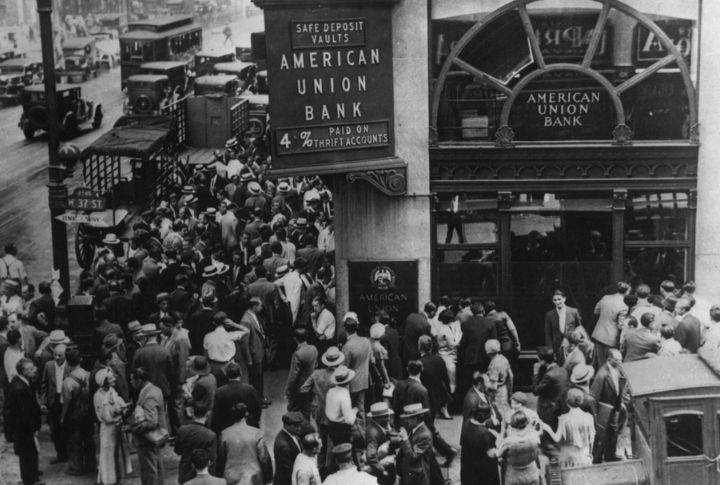

They Panicked During Bank Runs

The Great Depression triggered widespread financial instability, and one of the most devastating consequences was the collapse of banks. As economic uncertainty spread, fear took hold, and many middle-class Americans rushed to withdraw their savings. This mass withdrawal, known as a bank run, further destabilized financial institutions.

They Ignored Warning Signs Of Economic Trouble

Throughout history, financial crises have come with warning signs—yet few recognize them in time. Before the Great Depression, middle-class Americans underestimated growing risks. Stock market speculation, rising consumer debt, weak banking reserves, falling crop prices, and interest rate hikes all pointed to serious trouble. Still, these signals were largely ignored.