Filing taxes in retirement isn’t as simple as cashing a Social Security check. There are different forms for pensions, IRA withdrawals, and even specific tax rules for that side gig you picked up. Understanding these tax forms ahead of time can help save money and prevent penalties.

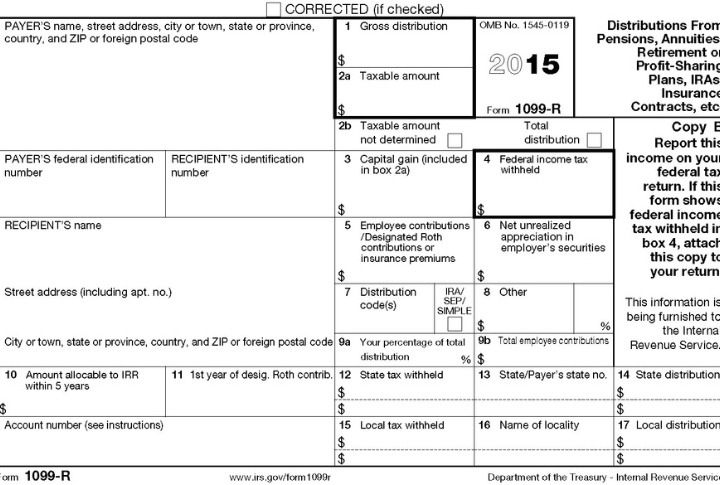

The 1099-R: Reporting Retirement Plan Distributions

If you withdrew money from a pension, annuity, 401(k), or IRA, the IRS wants to know about it. The 1099-R reports the amount you took out and whether taxes were withheld. Generally, retirement account distributions are considered taxable income. However, some withdrawals may be partially taxable if they include after-tax contributions. Yet, certain rollovers or direct transfers may not be taxable.

The SSA-1099: The Social Security Benefits Statement

Social Security benefits aren’t always taxable, but they might be if your total income crosses a certain threshold. If you’ve ever wondered why some retirees pay taxes on their Social Security while others don’t, this form holds the answer. The SSA-1099 reports how much you received in benefits.

The 1040: The One Form You Can’t Escape

No matter how simple or complex your retirement finances are, you’ll still need to file Form 1040. This is the primary tax return where everything comes together—income, deductions, and credits. While retirees may no longer deal with W-2s, they still have to report earnings from investments, benefits, and withdrawals.

The 1099-INT: Because Your Savings Account Earns Interest

Even a few dollars in interest from your bank account or CDs need to be reported, and the 1099-INT is how banks inform you (and the IRS) of what you earned. It might not seem like a big deal, but leaving it off your return could trigger an IRS notice later.

The 1099-DIV: If You Own Stocks, This One Matters

Dividends from stocks, mutual funds, or ETFs are reported on the 1099-DIV. Some are taxed at the lower capital gains rate, while others are taxed as ordinary income. Reinvesting dividends instead of cashing them out? You still need to report them. Don’t ignore this form when tax time rolls around.

The 5498: Keeping Track Of IRA Contributions

This one’s easy to overlook, but the IRS doesn’t miss it. Even post-retirement, some folks contribute to Roth IRAs or rollover accounts. Form 5498 shows how much you contributed, rolled over, or if you took the required minimum distributions. You don’t file it, but cross-check it—it’s the IRS’s receipt to ensure you’re playing by the rules.

The W-4P: Adjusting Tax Withholding On Pension And Annuity Payments

When those pension or annuity checks roll in, the W-4P is what decides how much tax gets skimmed off the top. Maybe you set it years ago and forgot about it. But if too little is withheld, a surprise tax bill could be waiting. It’s adjustable anytime, so it’s worth revisiting as your income changes.

The 8962: If You’re On Marketplace Health Insurance

If you retire before Medicare kicks in, you might rely on Marketplace health insurance. Here’s where things get tricky—premium tax credits are based on estimated income, but if you underestimate, the 8962 will square up the difference. It could mean extra money back or an unexpected tax tab to settle.

The 5329: If You Took An Early Withdrawal Or Missed An RMD

Did you take money out of a retirement account before age 59.5? Did you miss a required minimum distribution (RMD)? The IRS doesn’t just let that slide. Form 5329 calculates the penalty, sometimes up to 50% of the missed RMD! Thankfully, you can request a waiver if you have a really good reason.

The Schedule B: When You Have A Lot Of Interest And Dividends

The IRS wants extra details if you’re earning over $1,500 in interest or dividends. That’s where Schedule B comes in handy. It breaks down sources of income, so large interest payments or multiple brokerage accounts don’t go unnoticed. Forgetting this won’t necessarily lead to an audit, but it could delay your refund.